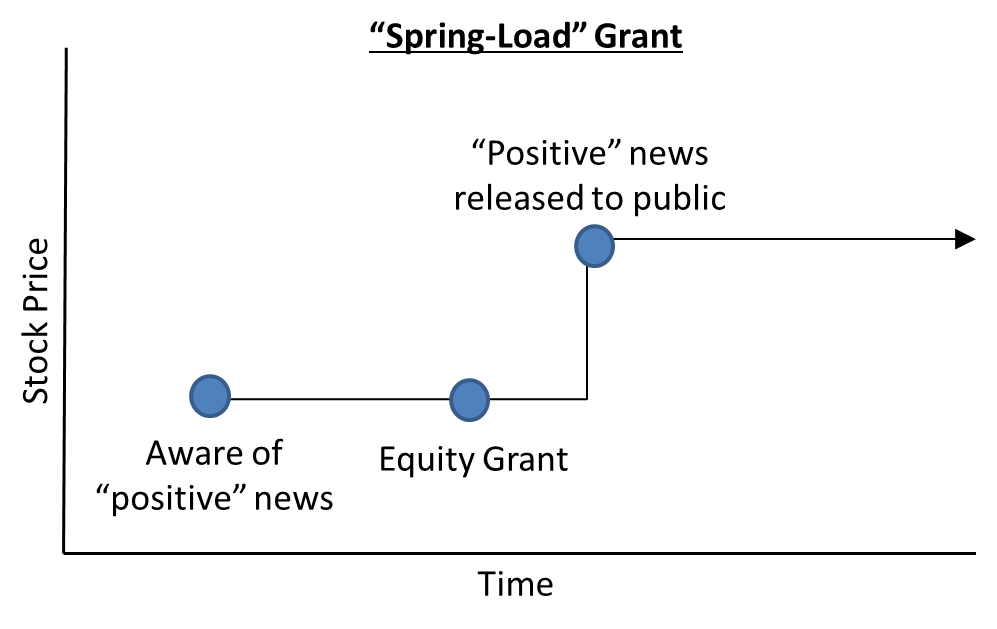

Spring-Load Vibes

NYSE: KVYO - Klaviyo

Klaviyo recently installed a new co-CEO at its helm and all signs point to the stock having limited downside, given the timing of the grant. Could it go as far as being a spring-load? Guess we’ll have to wait and see.

On December 8, 2025, Klaviyo appointed Chano Fernández to the co-CEO position, with an effective start date of January 1, 2026. With his appointment came a $69MM grant comprising RSUs and PSUs. Fernández had been on Klaviyo’s board since 2023, and was elevated to Interim Executive Officer in September 2025, likely setting up an eventual CEO succession.

The grant itself was summarized in an “Intention Letter” which contained the following details:

$33MM in RSUs vesting over three years

50% automatic vesting if terminated within 18 months for “cause” or for “good reason”.

100% vesting in a “sale event” if he continues service through to the closing date.

Number of RSUs granted = $33MM / 30-day average price of the stock ending on the effective date of the grant.

$36MM in PSUs

Based on the following stock price hurdles: $40, $55, $70, and $85.

5-year measurement period.

100% vesting if terminated within 18 months for “cause” or for “good reason”, assuming the stock price hurdles are met.

100% vesting in a “sale event” if he continues service through to the closing date, assuming the stock price hurdles are met.

Number of PSUs granted = $36MM / 30-day average price of the stock ending on the effective date of the grant.

On January 16, 2026, we finally got details on the amount of RSUs and PSUs issued to Fernández:

1,093,801 RSUs

1,193,238 PSUs

Share price hurdles of: $40, $55, $70, and $85.

The stock traded at ~$24 at the time of the grant.

Granted on January 15, 2026.

While the share price targets are staggering, I also happened to notice something interesting about the timing of the award.

Although Fernández’s appointment to co-CEO was effective January 1, 2026, the grant itself was made on January 15, 2026. This timing difference isn’t all that uncommon but the fact that Klaviyo typically announces Q4 results in mid-February is interesting. Why would the board wait a full two weeks after he was appointed to grant him equity? Is two weeks enough time to get a preliminary “insider” view of Q4 earnings? Would they have delayed the grant subsequent to Q4 earnings if the results were going to be bad?

Fernández’s RSU grant is very large, and most boards would want to ensure that they “get the timing right”. It’s in nobody’s interest for a $69MM grant to be made, and have the stock drop 20% a month later on bad results.

While the potential spring-load is a great short-term trade, the large amount of PSUs given to him with high price hurdles is definitely intriguing. Based on my searches, Klaviyo has never given executive grants with price hurdles such as these.

To present the counterargument of the long thesis:

Executives continue to sell into 10b5-1 plans, seemingly non-stop, and in large quantities.

There have been a few recent and large secondary sales:

May 2024 - Founder Andrew Bialecki (~10% of the shares he had prior) selling 10.9MM shares at ~$34.

August 2025 - Summit Partners (~22% of the shares they had prior) selling 6.5MM shares at ~$30.

Companies have shied away from spring-load grants since the SEC increased their scrutiny.

I’ll leave you with one powerful fact: Fernández was the chair of the compensation committee for two years until his appointment as Interim Executive Officer in September 2025.

“♡ Like” this piece to load that spring!